Credit…Its a Game

January 25, 2021

I love to play games. Credit is just another game that we play in our lives. Some know how to play and others dont. I can show you some tricks to play.

Credit is used to buy a car, furniture, a house and its also used when you buy car insurance and bunch of other ways that we will not even go into here.

GET a FREE Copy Of My Book!

10 Things Nobody Will Ever Tell You That You Need To Do To Invest In Real Estate.

Yes, car insurance. If you want to make payments every month, your credit will be pulled. If you go to Ashley Furniture to buy some new furniture on credit, they will pull your credit.

This is really important and can mean the difference in $1000s of dollars over a lifetime when you go to purchase a house. Good credit will save you some money, bad credit will cost you an arm and a leg.

So how can you save a bunch of money with good credit for you house, cars, furniture and everything else??

The first step in playing a game is to know the rules. So lets look at the rules that the credit card companies have set up for us.

The three credit rating companies, Experian, Equifax and TransUnion give everyone a score. This score is what companies pull to see if we humans are credit worthy. This magical score is always changing and will be different for different people who pull our score.

This magical score runs from 250 to 900 for one company, 350 to 850 for another. Roughly they are about the same. Whichever company gets your score if you have over 700 you are doing pretty good. Anything over 800 you will have probably the best mortgage rates, car loan rates, etc. When you go below 600 sometimes it gets hard to rent an apartment or even get a car with a 10% interest rate.

Why is it different when different companies pull our credit score? It depends on what you are buying. Mortgage companies want to see ALL of our credit. A car dealer may only want to know if we have a mortgage and other cars along with credit cards. A furniture store may only want to know if we pay our credit cards on time.

I say that the score is magical because no one knows exactly how we get our score. We can guess pretty good, but no one knows exactly how the companies score us. Every company that extends us credit has their own criteria for what they want to know about us. They will use different factors to determine if we are credit worthy.

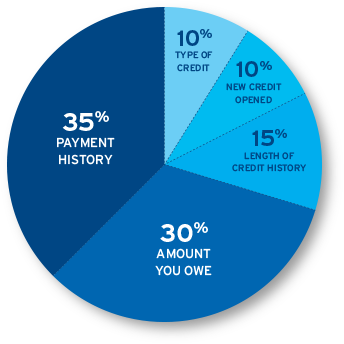

So there are 5 factors that are measured by the credit card companies. They are in order of importance: Payment history, Amount you owe, Length of credit history, new credit opened, and type of credit. Let me tell you a little about each factor and what you need to do with each one.

Payment History

This factor accounts for about 35% of our credit score.

This is pretty simple. Do you pay your bills on time. Experian and the others keep track of whether or not you have paid your bills on time. Your history of paying is a pretty strong indicator if you are going to continue paying your bills on time. This is why it is given more weight in your credit score.

This is really the easiest way to keep your credit score up, pay your bills on time. If you pay some bills late, your score will go down.

Amount You Owe

This one accounts for 30% of your score and is a little tricky.

It is really the amount that you owe compared to how much credit that you have. Let me give you an example. If you owe $1000. That does not seem too bad. BUT if you have a total credit limit on your credit cards of $1000, you are completely at your limit and at 100%, not good.

On the other hand, if you have a total credit limit of $20k and you owe $1000, not a big deal at all. Your percentage is only at 5%. Very low and very favorable when it comes to lending money.

The credit companies say that it is best if you owe less than 10% of your limit. The lower that percentage is, the better. Sometimes you can bump up your credit score by opening another credit card with a high limit which will increase your total limit.

Again lets say that you owe $1000 and you have only 5 credit cards with a total of $1000 limit. You apply and get a new credit card with a $5000 limit. Now you have $6000 limit and owe $1000. Now you are at 16.6% of your limit which is pretty good. Your credit should go up. And of course as you pay it down, your score should go up also.

Length of Credit History

This one is less important and accounts for about 15% of your credit score. Its a little tougher though.

The credit companies want you to have your credit for 7-8 years or optimally 9 years+. Obviously for someone who is 20 or even 25 who has had credit for a few years is impossible.

Plus if you cancel a credit card that you have had for a while, the average age of your credit goes down. This is kinda crazy in my case. I had a few credit cards a bunch of years ago that were way high interest rate and had high annual fees. Well I did what I thought was a good idea and got rid of them. It kinda was, and kinda wasnt.

Since they were no longer a part of my credit history, my age of credit or length of credit history went way down. Right now I have about 6 years average. I ended up keeping one card that I have had for 12 years. It has a $35 annual fee which I dont like, but if I cancel that one, my average age will probably drop along with my score. I will probably keep it a few more years and then get rid of it.

When you have have a bunch of credit cards that are under 4 years, you are considered a high risk because you have not had credit for a long enough time. Its like a kid with something new. They think you might not know how to handle your credit yet. As time goes by, the credit card companies believe that you will become seasoned and able to handle your credit.

New Credit Opened

This one has less impact at only about 10% of your credit score.

Credit inquiries is also what this is called. If you have lots of people pulling your credit it usually means that you are trying to get lots of credit. That is not what the credit card companies want you to do all at once. They allow you to have 2 credit inquiries on your credit and still be in good standing.

These inquiries stay on your credit report for about 2 years. To keep this at a minimum, I get some sort of credit every year which means that I always have one or two inquiries on my credit report at all times. I am also increasing my credit which should help my score go up.

I have been doing this for the last few years and have managed to increase my available credit to over $80,000. Of course I dont owe that much and I can not imagine ever owing that much, but it is available. Again, they think that if you have it and dont use it, that shows restraint and makes you worthy of a better credit score.

Type of Credit

This is one that I find kind of crazy, but luckily it only accounts for 10%

They want you to have a variety of types of credit. They want you to have a car loan, house loan, and some credit cards. It sounds good in theory, but what if you pay off your house?? What if you dont have a car payment??

That is what happened to me. I paid off my house. Sounds good right? I owed about $70k on a $85k mortgage, so I thought the amount I owed would go down dramatically. It did. But my credit score went down too. Womp womp.

Right now I have my new house loan with a friend. They lent me money for my house because I was doing repairs on it and could not get a regular mortgage. Actually my mortgage does not show up on my credit at all. That should be great, but since I only have some credit card debt, it says that I dont have a house loan or a car loan.

You would think that the credit scoring companies would want me to pay off my car and house, right? Well they dont. They want you to owe everyone!!

Over time, my score has gone back up with good pay history and low credit card utilization, but I think it will go even higher when I get a newer car. The problem is that I dont really want to buy a new car.

As of now my credit score is in the mid to high 700s. That is a great score to get a new credit card that has a bunch of points along with it, like the Chase Sapphire Preferred It always has several hundred dollars worth of points when you spend several thousand dollars in the first 3 months.

That works out great for me because I am always doing a rehab and I end up spending several thousand dollars every week or two.

As I have mentioned before, you have to keep track of things. I keep track of my weight, net worth, my projects that I am working on, my credit score and my goals. While I do check on different items at different times, I do track them and make sure they are moving in the right direction.

For my bike riding I use Strava. For my weight, I check the scale every morning. My credit is checked every week with Credit Karma. It is very quick and easy to set up and most of all it does NOT affect your credit to check your credit. Also, its free. Free is ALWAYS good.

You can always get your free credit report once per year from each of the 3 credit bureaus. Did I mention that I like FREE?? Take care of your credit and your credit will take care of you. Be Frugal My Friends.